What Are the Costs of Filing for Bankruptcy in Canada?

Thinking about bankruptcy to ease your debt load? If you are exploring this option, you are probably wondering, how much does it cost to file for bankruptcy in Canada? Getting a clear answer can make the process feel less intimidating, and that is exactly what we are here for.

Let’s break down what you will be looking at, the factors that impact the cost, and how you can manage it without breaking a sweat.

What Are the Basic Costs of Filing for Bankruptcy?

Bankruptcy fees in Canada are not exactly one-size-fits-all, but here are the main costs you can expect:

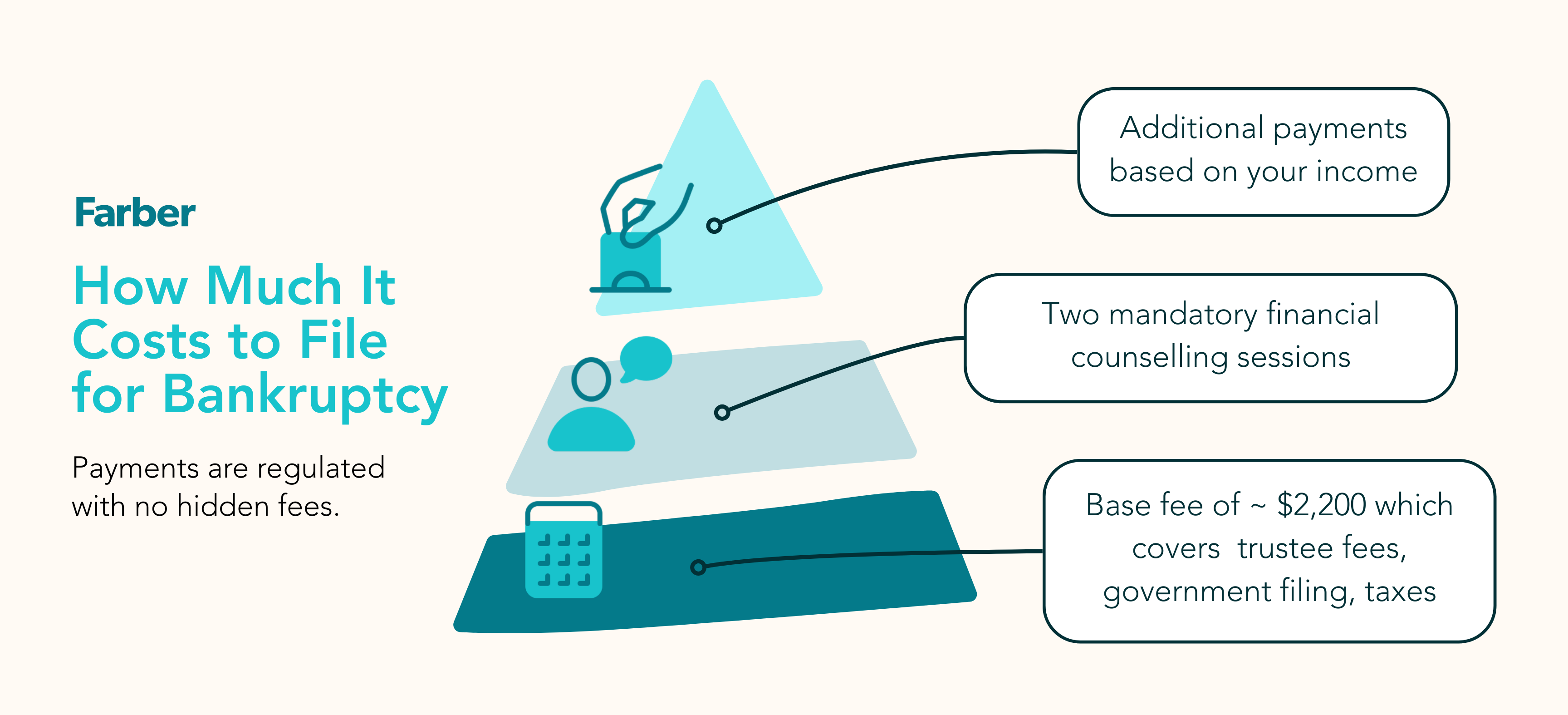

Starting Cost

Filing for bankruptcy for the first time usually starts with contributing $2,200, but do not worry—most people can pay this overtime, for example, equal payments over a nine-month plan. This amount covers the basics, like administration, filing fees, counselling fees, taxes for goods and services, and basic trustee fees that are allowed according to the tariff set by the government. It is pretty much the foundation of your bankruptcy payments.

Trustee Fees and Disbursements

In Canada, filing for bankruptcy involves working with a Licensed Insolvency Trustee (LIT). This professional is your go-to to guide you through the process, handling everything from filing the paperwork to dealing with creditors. Trustees are government-regulated, so their fees and disbursements are part of your total payments to your bankruptcy and are consistent across Canada. This way you are not getting hit with random or extra payments that are not according to the rules.

Additional Payments If You Are Above a Certain Income

If you are earning more than a set amount each month (think $2,610 for a single person), you might need to pay a little more. Basically, if your monthly income is above the allowed amount, you will need to put part of that extra cash toward your bankruptcy. But if you are not making more than the limit, you do not have to worry about this part.

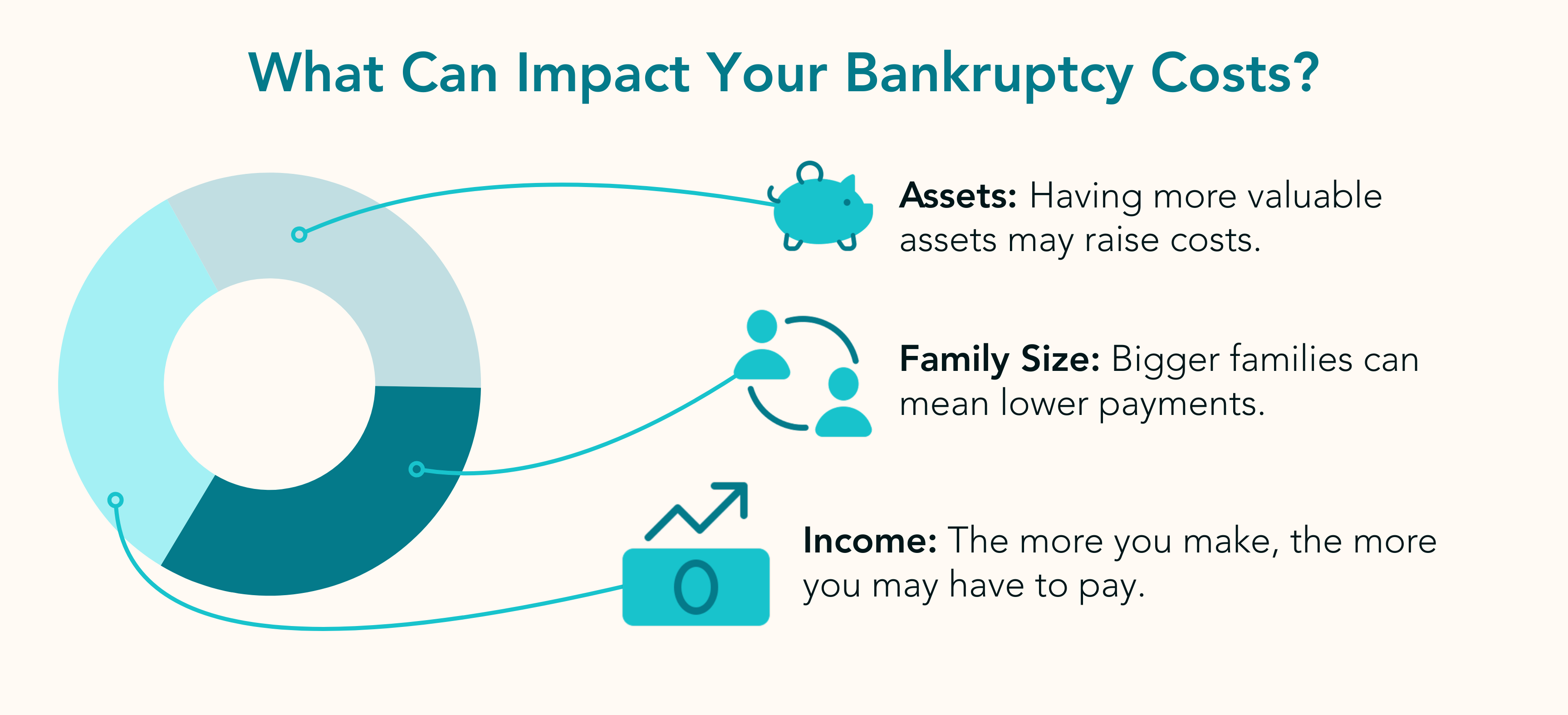

What Can Make Your Bankruptcy Costs Higher or Lower?

Bankruptcy costs are not the same for everyone. A few things can shift the amount up or down, so let’s break down the main factors:

- How Much You Earn: As mentioned, if your income is above a certain level, you will likely have to make additional payments each month. The government sets these income levels based on household size, so a single person has a lower income cap than a family of four, for example.

- Your Family Size: As we mentioned above, larger households have higher income caps before extra payments are required. This helps account for the fact that a family of four obviously has higher living costs than a single person.

- Assets You Own: If you have high-value items like a second home, a fancy car, or expensive jewelry, you may need to give them up or pay for their value as part of the process to keep possession of them. Some assets are protected—think basic home goods and a modest car—so you will not lose everything.

The Main Bankruptcy Fees (and What They Actually Cover)

Here’s a closer look at the core fees you will be dealing with if you file for bankruptcy:

Trustee Fees and Disbursements

This is a big part of the cost of filing for bankruptcy. Your LIT is there to make sure your case goes smoothly, handle your paperwork, file legal documents, deal with your creditors, and guide you through the process. Since their fees are regulated across Canada, you are not looking at any surprise add-ons, and they are typically included in the overall base amounts you have to pay.

Mandatory Counseling Sessions

The bankruptcy process requires you to attend two financial counselling sessions. Think of these as little workshops to help you build better money habits, so you do not find yourself back in debt later. They are usually part of your overall cost but check with your trustee to confirm.

Additional Payments Based on Income

As we mentioned, if you are earning over a certain amount, the government may ask you to make extra monthly payments. For example, if you are a single person making a net income of $3,110 a month, you would pay half of the amount over $2,610 (the monthly limit) toward your bankruptcy over a period of several months.

Watch Out for a Few Extra Costs

Along with the main fees, a few smaller costs might pop up along the way. Here are some additional things to keep in mind:

- Giving Up Certain Assets: If you own anything valuable that is not considered essential like high-value jewelry or a second property, you may need to hand it over or pay its equivalent value to cover your debts to keep the asset.

- Tax Refunds: During the bankruptcy period, any tax refunds you are eligible to receive for the year of your bankruptcy, might go directly toward paying off your debt instead of coming back to you.

- Changes in Income: If your income goes up while you are in bankruptcy, you may have to increase your monthly payments. This does not happen for everyone, but it is something to keep in mind if your financial situation shifts.

Tips for Handling Bankruptcy Costs

We get it—bankruptcy costs can feel like just one more financial hurdle. But there are ways to make it manageable. Here is how:

- Start Saving a Little Each Month: Even if you are on a tight budget, putting aside a small amount each month can help cover those initial costs when you are ready to file.

- Ask About Payment Plans: Many trustees offer payment plans for the base amounts required, so you can spread out the payments over several months instead of paying it all at once.

- Cut Back on Non-Essentials: Small changes, like eating out less or pausing a few subscription services, can add up and help you save for the required payments.

Balancing the Costs with the Benefits

Yes, filing for bankruptcy comes with costs, but it is also a way to finally move forward without that overwhelming debt dragging you down. Balancing these costs with the chance for a fresh financial start can help you decide if this is the right step for you. And remember, if bankruptcy does not seem like the best fit, other options—like consumer proposals—might make more sense for your situation.

How Farber Can Help

If bankruptcy is on your mind, Farber’s Licensed Insolvency Trustees are here to help you sort through the details and explain the costs step-by-step. From payment plans to alternative options like consumer proposals, we are here to guide you and answer any questions you have. Ready to take the next step? Book a free consultation with one of our experts to talk about the best options for you.

Filing for bankruptcy in Canada can seem like a big commitment, but with a bit of planning and the right support, you can handle the costs and look forward to a brighter financial future!

Get out of debt

We offer a powerful debt-relief solution that can significantly reduce your debt without the drawbacks of declaring bankruptcy.

Take the first step

Book a free, confidential, no-obligation consultation and together, we can make a plan to help regain control of your money.

What you need to know

Although debt can be overwhelming, there are ways to start fresh and improve your relationship with money.